Blog

The Roth IRA Conversion 5-Year Rule: How the Two Clocks and the Age 59 1/2 Exception Work Together

The Roth IRA conversion 5-year rule and the Roth earnings 5-year rule are two different clocks with two different jobs, and confusing them can trigger a surprise 10% penalty. This guide breaks down both rules, the IRS distribution ordering rules, and exactly how the age 59 1/2 exception changes the math.

Anyone who converts a traditional IRA to a Roth IRA eventually runs into "the 5-year rule." The trouble is that there are actually two of them, and they answer different questions. One clock decides whether your investment earnings come out tax-free. The other decides whether the money you converted can come out without a 10% penalty. Mixing them up is one of the most common (and costly) mistakes people make when tapping a Roth IRA early.

This matters even more for people using a self-directed IRA to hold alternative assets like pre-IPO stock, private business interests, or real estate, since conversions of those assets often involve larger balances and more complex timing decisions. Understanding both clocks, and how the age 59 1/2 exception interacts with them, is essential before you convert or withdraw anything.

What Is the Roth IRA Conversion 5-Year Rule?

The Roth IRA conversion 5-year rule is a separate waiting period attached to each individual conversion, not to your Roth IRA account as a whole. Its clock starts on January 1 of the tax year in which that specific conversion occurs, and it exists to determine whether the converted amount can be withdrawn without triggering the 10% early distribution penalty.

Here is the part that trips people up: every conversion you make gets its own 5-year clock. If you convert money in 2023 and again in 2025, you have two separate clocks running, and each one has to be tracked individually if you plan to touch that money before age 59 1/2.

The Two Clocks: Earnings Rule vs. Conversion Rule

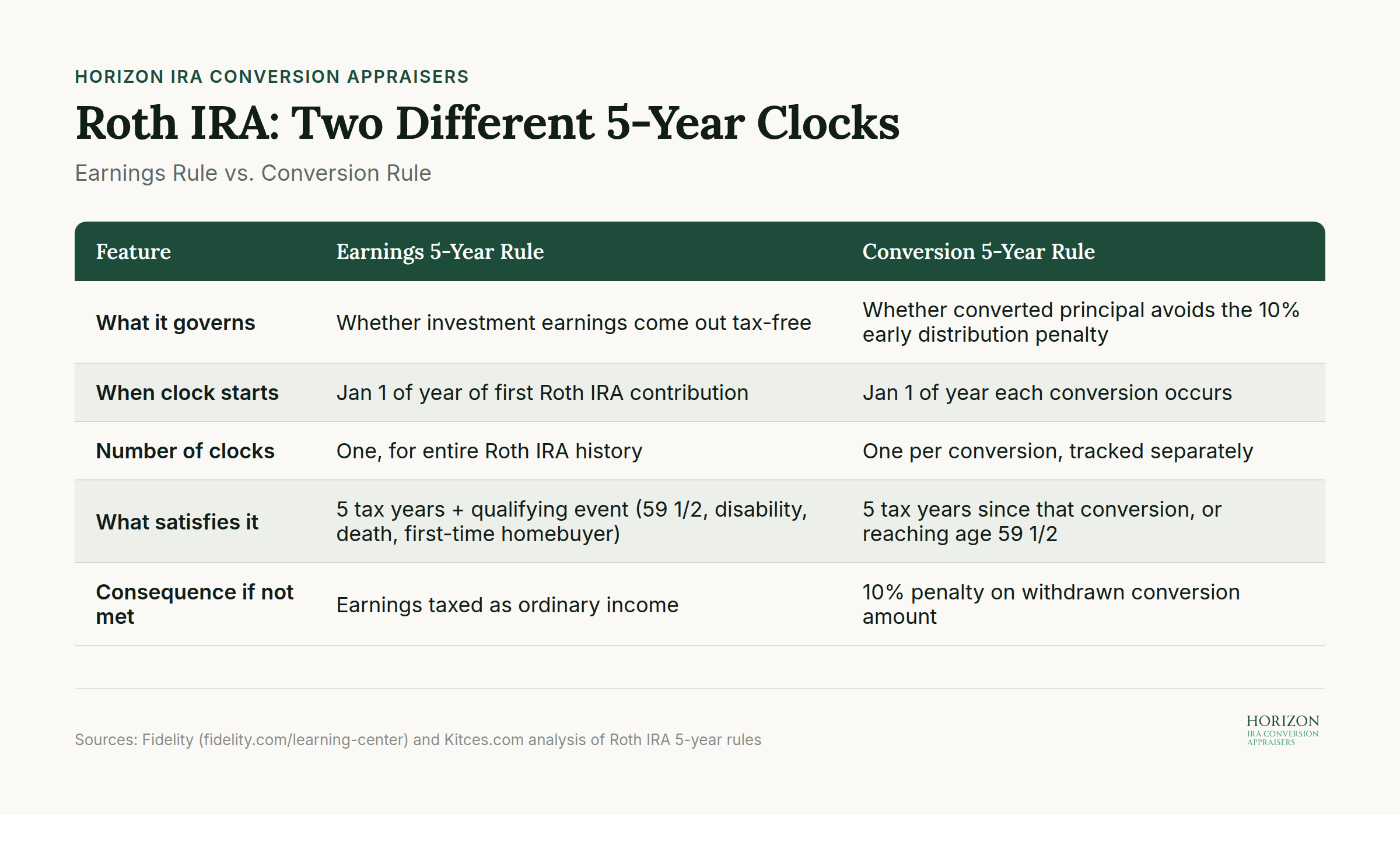

The earnings 5-year rule and the conversion 5-year rule sound similar but govern completely different things. Confusing the two is the single biggest source of Roth withdrawal mistakes, so it helps to see them side by side.

| Earnings 5-Year Rule | Conversion 5-Year Rule | |

|---|---|---|

| What it governs | Whether investment earnings come out tax-free | Whether converted principal avoids the 10% early distribution penalty |

| When the clock starts | January 1 of the year of your first Roth IRA contribution (any Roth IRA, contribution or conversion) | January 1 of the year each individual conversion occurs |

| How many clocks you have | One, for your entire Roth IRA history | One per conversion; each has its own separate clock |

| What satisfies it | 5 tax years elapsed, plus a qualifying event (age 59 1/2, disability, death, or first-time homebuyer) | 5 tax years elapsed since that conversion, or reaching age 59 1/2 |

| Consequence if not met | Earnings are taxed as ordinary income | Withdrawn conversion amount owes a 10% penalty |

According to Fidelity, the IRS requires this 5-year waiting period before amounts converted from a traditional IRA can be withdrawn without triggering the 10% early withdrawal penalty. Kitces frames it clearly: one rule protects the tax-free status of earnings, the other protects the Treasury from people using Roth conversions to sidestep the early distribution penalty altogether.

A key point often missed: the conversion clock has nothing to do with income tax on the conversion itself. You already paid ordinary income tax on the converted amount in the year you converted it, since that tax is due regardless of when you eventually withdraw the funds. The 5-year conversion clock is purely about the 10% penalty, not about income tax owed.

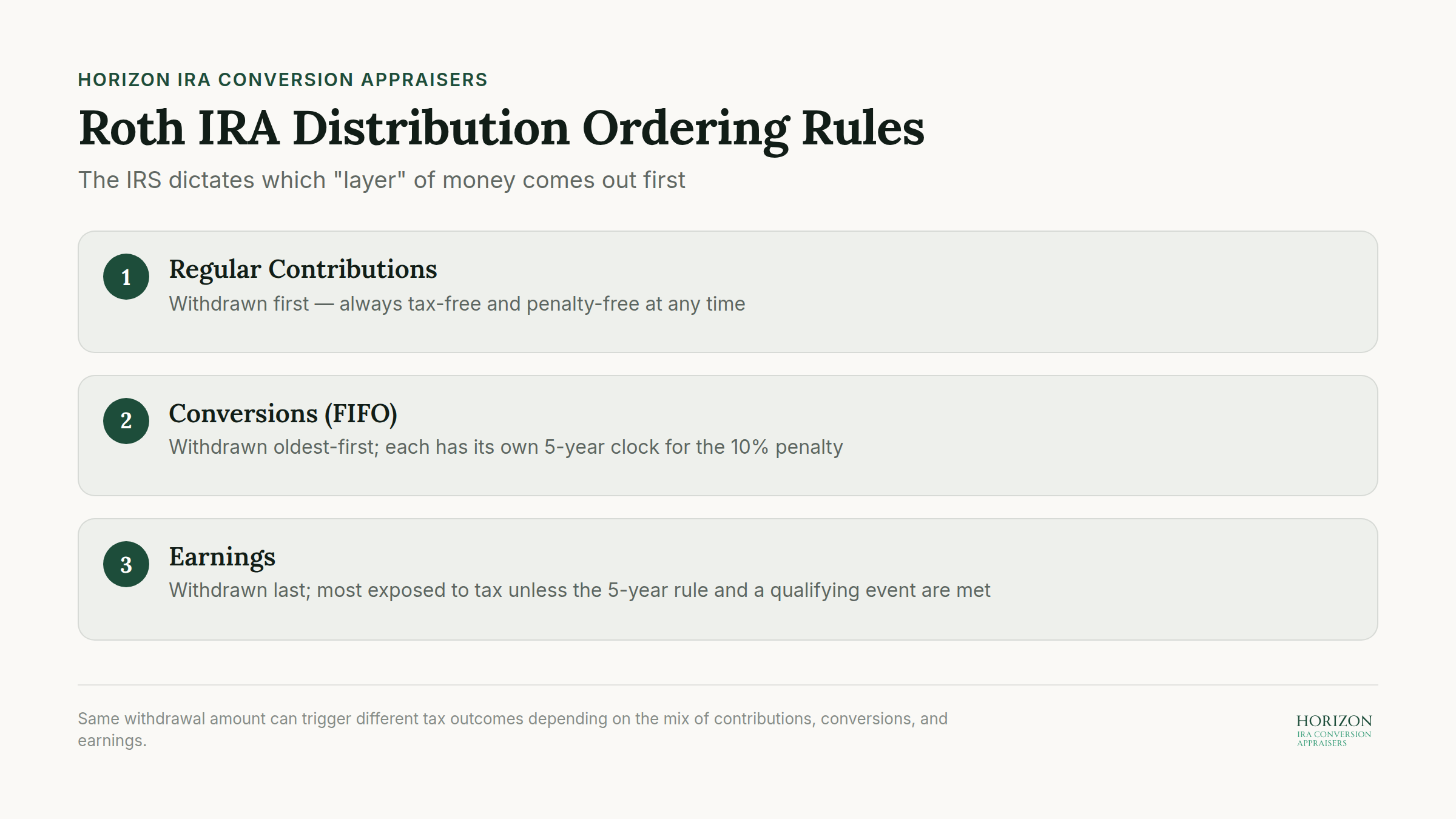

How the IRS Ordering Rules Work for Roth Distributions

When you take a distribution from a Roth IRA, the IRS does not let you choose which "layer" of money comes out first. Instead, distributions follow a strict ordering sequence that determines exactly what is taxed and what is exposed to a penalty.

- Regular Contributions Come Out First

- Direct contributions you made to the Roth IRA are always considered withdrawn first, and they come out tax-free and penalty-free at any time, since you already paid tax on that money before contributing it.

- Conversions Come Out Next, on a First-In-First-Out Basis

- Once contributions are exhausted, converted amounts are treated as withdrawn in the order they were converted, oldest conversion first. Each conversion carries its own 5-year clock, so the age of the specific conversion being withdrawn is what matters for the 10% penalty.

- Earnings Come Out Last

- Only after all contributions and all converted principal have been withdrawn do earnings start coming out. Earnings are the layer most exposed to tax if the account has not satisfied the earnings 5-year rule and a qualifying event.

This ordering sequence is why two people can withdraw the exact same dollar amount from a Roth IRA and face completely different tax consequences, depending on how much of their balance is contributions, conversions, or earnings at the time of the withdrawal.

The Age 59 1/2 Exception: What Changes and What Doesn't

Once you reach age 59 1/2, the 10% early distribution penalty tied to the conversion 5-year clock generally stops applying, even if the specific conversion has not been in the account for a full five years. This is the exception most people rely on to simplify their planning, since it means the conversion clock effectively becomes irrelevant once you cross that age threshold.

But age 59 1/2 does not automatically make the account's earnings tax-free. That still depends on the separate earnings 5-year rule. If your first Roth IRA contribution or conversion was made less than 5 years ago, earnings withdrawn before that 5-year mark are still taxable as ordinary income, even though there is no 10% penalty once you are past 59 1/2. Schwab and Wells Fargo both confirm this distinction: age solves the penalty problem, but the earnings clock is a separate hurdle entirely.

Watch out: People often assume that hitting 59 1/2 means their whole Roth IRA is "unlocked" tax-free and penalty-free. That is only true once both clocks are satisfied. If you are 60 years old but only opened your first Roth IRA 3 years ago, earnings withdrawn today are still taxable, just not penalized.

Worked Example: Converting $50,000 at Age 50

Here is how the two clocks play out with real numbers.

Example: Maria is 50 years old and converts $50,000 from a traditional IRA to a Roth IRA in 2024. She pays ordinary income tax on the full $50,000 that year, as required for any Roth conversion. Her Roth IRA had no prior contributions, so this conversion also starts her earnings clock (assuming this is her first Roth IRA).

Three years later, in 2027, Maria is 53 and decides she needs $20,000 from the account. Because her conversion clock started January 1, 2024, only 3 years have elapsed, not the required 5. She is also well under age 59 1/2, so the age 59 1/2 exception does not help her.

Under the IRS ordering rules, the $20,000 withdrawal is treated as coming from her converted principal (assuming she has no regular contributions in the account). Because the conversion has not met its 5-year clock and Maria is under 59 1/2, the withdrawn $20,000 is subject to the 10% early distribution penalty, or $2,000. She does not owe additional income tax on this $20,000, since she already paid tax on it at conversion; the penalty is the only consequence here.

Now compare that to Maria waiting until 2029 (5 full years after the conversion) or until she turns 59 1/2, whichever comes first. At that point, the same $20,000 withdrawal comes out with no 10% penalty at all, because either the conversion clock has been satisfied or the age exception applies.

Pro tip: If you are converting substantial assets, such as private stock or other alternative holdings inside a self-directed IRA, track each conversion's date separately in writing. With multiple conversions across different years, it is easy to lose track of which dollars are penalty-free and which are not.

Why This Matters for SDIRA and Alternative Asset Conversions

The stakes around these clocks rise significantly when the converted asset is not cash but something like pre-IPO stock, real estate, or a private business interest held in a self-directed IRA. A conversion of an illiquid asset locks in a tax bill based on its appraised fair market value at the time of conversion, and that value cannot simply be adjusted later if the asset's price changes. Getting the valuation right at the moment of conversion, and understanding exactly when the resulting funds become accessible without penalty, are both critical pieces of the same planning decision.

This is especially relevant for anyone converting discounted or restricted private stock positions, where the appraised conversion value directly drives both the tax bill and the size of the converted principal now subject to its own 5-year clock. Readers evaluating a private stock appraisal for an IRA conversion should treat the valuation date and the conversion date as two decisions that need to be made together, not separately.

Frequently Asked Questions

Q: If I am over 59 1/2, do I still need to worry about the 5-year rule? It depends on which withdrawal you are making. The conversion 5-year rule stops mattering once you are 59 1/2 or older, since the penalty it protects against no longer applies. The earnings 5-year rule can still apply if your first Roth IRA contribution was made less than 5 years ago, in which case earnings withdrawn are taxable even though no penalty applies.

Q: Does each Roth conversion really have its own separate 5-year clock? Yes. Every conversion is tracked individually from January 1 of the year it occurred. If you convert money in three different years, you have three separate 5-year clocks running simultaneously, as confirmed by guidance from Wells Fargo and Kitces.

Q: Do I owe income tax again if I withdraw converted funds before 5 years are up? No. You already paid ordinary income tax on the converted amount in the year of conversion. Withdrawing it early before the conversion's 5-year clock is satisfied (and before age 59 1/2) triggers only the 10% penalty, not additional income tax.

Q: What starts the earnings 5-year clock if I have never made a regular Roth contribution, only conversions? The earnings clock still starts on January 1 of the year of your first Roth IRA transaction, whether that transaction was a contribution or a conversion. It is not restricted to regular contributions.

Plan Your Conversion Timeline Before You Move Assets

The conversion 5-year rule and the earnings 5-year rule protect against two different risks: an early withdrawal penalty on converted principal, and premature taxation of investment gains. Age 59 1/2 resolves the first issue but not always the second, so tracking both clocks matters even after you clear that age milestone. For anyone converting alternative assets such as private company stock into a Roth IRA, getting the conversion-date valuation right is just as important as tracking the resulting 5-year clocks. If you are weighing a Roth conversion involving privately held or hard-to-value assets, our request an appraisal page walks through what a defensible conversion-date valuation involves and how it fits into your broader tax timeline.

This article is provided for general informational purposes only and does not constitute legal, tax, or financial advice. Readers should consult a qualified attorney or CPA regarding their specific circumstances.