Blog

What Is a Discounted Roth IRA Conversion and How Do Valuation Discounts Work?

A discounted Roth IRA conversion uses an independent appraisal to establish a defensible, discounted fair market value for illiquid self-directed IRA assets, so conversion tax is paid on that lower number instead of the nominal invested amount. This guide explains which assets qualify, how the discount is calculated, and what documentation the IRS expects to see.

What Is a Discounted Roth IRA Conversion?

A discounted Roth IRA conversion is a strategy available to self-directed IRA (SDIRA) owners holding illiquid, non-publicly-traded assets: private LLC or LP interests, direct real estate, or closely held business interests. Instead of converting at a rough estimate or the original invested amount, the account owner engages an independent, credentialed appraiser to determine the asset's fair market value (FMV) at the time of conversion. Because these interests are illiquid and often lack control over management or sale decisions, a properly supported appraisal can apply recognized valuation discounts, typically for lack of control and lack of marketability, before the conversion is executed.

The tax on the conversion is then based on that appraised, discounted value rather than the nominal or invested value of the asset. Once the asset sits inside the Roth IRA, future appreciation on that same interest is not taxed, provided ordinary Roth distribution rules are eventually met. For background on how SDIRAs hold these asset types in the first place, our self-directed IRA guide covers the structure in more detail.

This only works for assets the market cannot price on its own. If an SDIRA holds publicly traded stocks, ETFs, or mutual funds, there is no discount to apply. The market sets FMV every trading day, and that price is the conversion value, full stop.

How Roth Conversions Are Taxed in the First Place

A Roth conversion is treated as a taxable event valued at the fair market value of the assets converted on the date of conversion. The IRS does not care what you originally paid for the asset or what you believe it might be worth someday; it cares what the asset is worth, supportably, right now.

For publicly traded holdings, that number is easy: the closing price on the conversion date. For an LLC interest in a family real estate venture, a fractional stake in a rental property, or shares in a closely held operating company, there is no ticker to check. That FMV has to come from somewhere defensible, which is where an independent appraisal enters the process. According to Anchor 1031's overview of the strategy, the declared FMV of the converted asset is what drives the entire tax bill, which is exactly why the valuation has to hold up.

Watch out: Estimating a value yourself, or accepting a number from the fund sponsor or promoter who sold you the investment, is not the same as an independent appraisal. Both practices invite scrutiny and neither produces a report an appraiser would stand behind if the IRS asked questions. For more on the mechanics of when tax is actually owed, see when you pay taxes on Roth IRA conversions.

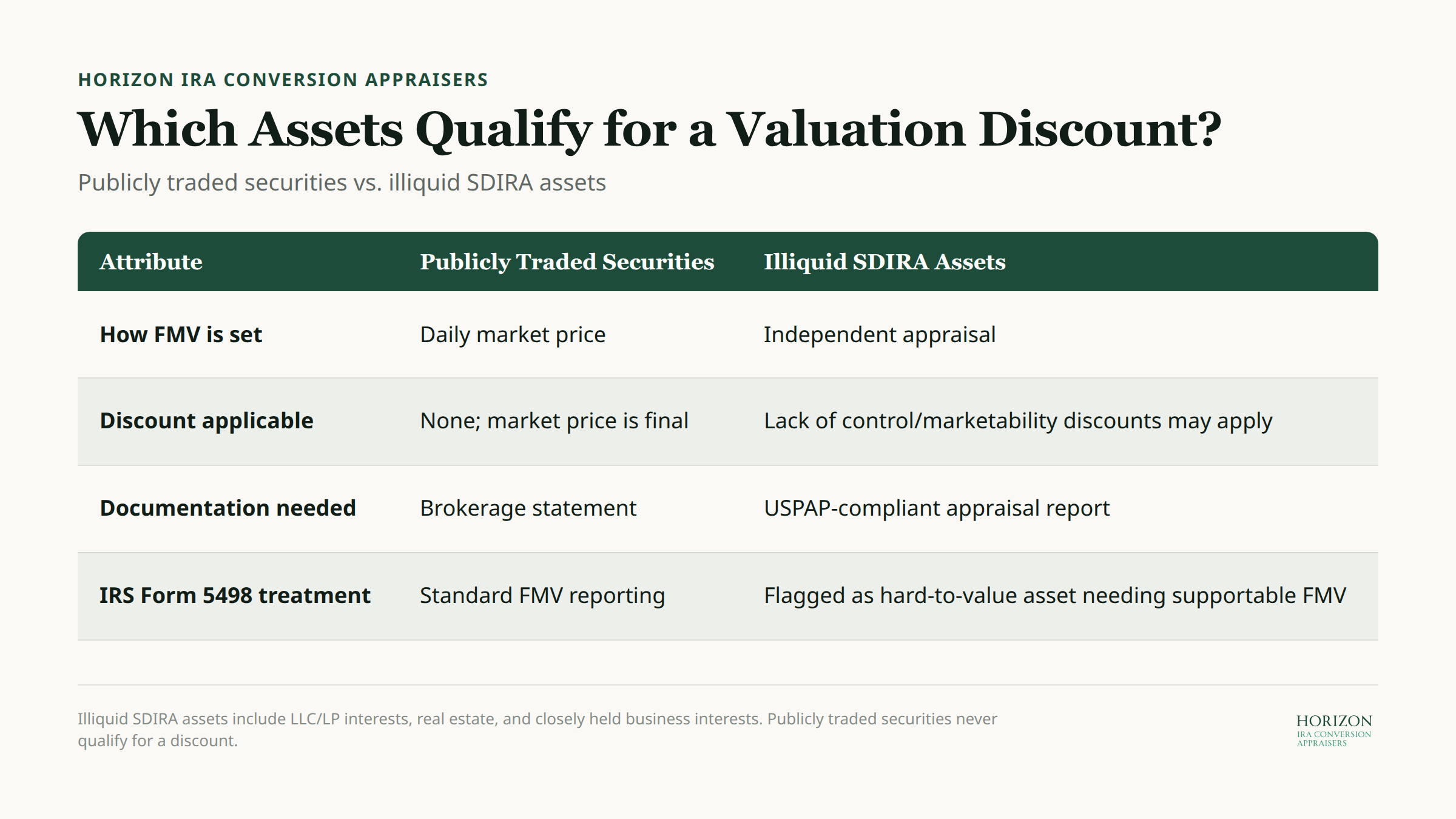

Which Assets Qualify for a Valuation Discount?

The short answer: illiquid, privately held interests where no active market sets the price. Publicly traded securities never qualify, because their FMV is already fixed by market transactions and cannot legitimately be discounted.

Assets commonly involved in discounted Roth conversions include:

Private LLC or LP interests: ownership stakes in real estate syndications, private funds, or operating businesses held through an SDIRA.

Direct or fractional real estate: rental property, land, or a partial interest in real property where transfer restrictions or co-ownership limit liquidity. If you're weighing whether property belongs in an IRA at all, can you hold real estate in a Roth IRA walks through the basics.

Closely held business interests: minority stakes in family businesses or private companies with no ready buyer and no public market.

The table below outlines why illiquid assets can be discounted while publicly traded holdings cannot.

Attribute | Publicly Traded Securities | Illiquid SDIRA Assets (LLC, real estate, private business) |

|---|---|---|

How FMV is set | Daily market price | Independent appraisal |

Discount applicable | None; market price is final | Lack of control and lack of marketability discounts may apply |

Documentation needed | Brokerage statement | USPAP-compliant appraisal report |

IRS Form 5498 treatment | Standard FMV reporting | Flagged as a hard-to-value asset requiring supportable FMV |

How Valuation Discounts Actually Reduce the Taxable Amount

A valuation discount lowers the appraised FMV of the asset, and since conversion tax is based on FMV, a lower appraised value means a lower tax bill in the year of conversion. This is not a loophole; it reflects the same lack of control and lack of marketability discounting long used in gift and estate tax appraisal, applied here to a conversion instead of a transfer.

Discounts for lack of control (sometimes called minority interest discounts) account for the fact that a non-controlling owner cannot force a sale, direct management, or dictate distributions. Discounts for lack of marketability account for the absence of a ready buyer and the time and cost involved in exiting the position. Courts and appraisers have historically supported combined discounts in the 20% to 40%-plus range for minority, illiquid interests, when the underlying legal agreements (an LLC operating agreement restricting transfer, for example) support that conclusion, according to industry commentary from Matthew Chancey on discounted Roth conversion planning.

Example: Suppose an SDIRA holds an LLC interest that might be worth $200,000 based on the underlying asset's pro-rata share of equity. An independent appraiser, applying supportable lack of control and lack of marketability discounts, concludes the interest's fair market value is $140,000, a 30% combined discount. The IRA owner converts that interest to a Roth IRA. Taxable income for the conversion is $140,000, not $200,000. At a 24% marginal rate, that is $33,600 in tax instead of $48,000, a $14,400 difference. From that point forward, any growth in the interest's actual value happens inside the Roth IRA and is not taxed again at distribution, assuming Roth rules are met.

A real-world variant of this shows up with construction-stage real estate, where an interim appraisal during the build phase can reflect meaningfully lower value than the stabilized, completed project, as described in BV Capital's discussion of Roth conversions using real estate. Converting at that interim, lower valuation shifts more of the eventual appreciation into the Roth IRA's tax-free growth.

Form 5498 and IRS Reporting on Hard-to-Value Assets

Custodians are required to report the fair market value of every asset in an IRA every year, including illiquid holdings that lack a readily available market price. On the annual reporting form, hard-to-value assets like LLC ownership interests (unless traded on an exchange) and real estate are specifically flagged as assets lacking a readily determinable FMV, which is exactly the category discounted conversions fall into. The IRS requires custodians to obtain and report a supportable value for these holdings, not a placeholder or an estimate carried over from the prior year.

This reporting requirement is precisely why the appraisal matters so much. The value used for Form 5498 reporting and the value used to calculate conversion tax should be the same defensible number, produced by the same independent process.

"In a Roth conversion, the declared fair market value of the asset drives the immediate tax bill. Undervalue it, and you pay less tax, but potentially invite IRS scrutiny." - Encore Retirement, on discounted Roth conversions

Key takeaway: The discount only works in your favor if it is documented well enough to survive that scrutiny. A number pulled from thin air is a liability, not a strategy.

Who Should Actually Consider This Strategy?

Discounted Roth conversions make the most sense for larger IRAs holding genuinely illiquid assets, where the potential tax savings clearly outweigh the cost of a professional appraisal and any legal review of the underlying agreements. For a small account or a marginal discount, the appraisal fee alone may erase the benefit.

A few practical realities to weigh before pursuing one:

You need outside cash to pay the tax. Conversion tax is due in the year of conversion, and it generally cannot be paid from IRA funds without triggering additional distribution consequences. If you don't have non-IRA cash available, a discounted conversion may not be practical regardless of how favorable the appraisal is.

The discount has to be defensible. A 20% to 40%-plus combined discount is well established in appraisal practice, but it has to be supported by the specific facts of your asset, including operating agreements, transfer restrictions, and comparable market data, not just asserted.

The appraiser needs to be independent. A valuation prepared by the fund sponsor, the LLC manager, or anyone with a financial stake in the outcome carries far less weight than one prepared by a credentialed, unaffiliated appraiser.

Pro tip: Line up the appraisal before you commit to a conversion date. Illiquid asset valuations take time to prepare properly, and rushing the process tends to produce weaker documentation, which defeats the purpose of getting an appraisal at all.

Why the Appraisal Needs to Be Independent and USPAP-Compliant

At Horizon Business Valuations, our appraisers prepare independent fair market value appraisals for the SDIRA assets most often involved in discounted conversions: LLC interests, direct and fractional real estate, and closely held business interests. Every report is prepared in accordance with the Uniform Standards of Professional Appraisal Practice (USPAP), published by The Appraisal Foundation, and our valuation team includes credential holders recognized by organizations such as the American Society of Appraisers and NACVA.

A USPAP-compliant appraisal does not guarantee the IRS will accept any particular discount; that determination rests with the IRS, not with us. What it does provide is a defensible, methodologically sound record of how the value was reached, prepared by someone with no financial interest in the underlying asset. That independence is the entire point. If you're weighing a related strategy involving private company stock rather than real estate or an LLC, our guide to private stock appraisal for IRA conversions covers that scenario specifically.

Frequently Asked Questions

Q: Can I apply a valuation discount to stocks or mutual funds in my IRA? No. Publicly traded securities have a market-determined price on any given day, and that price is the fair market value used for conversion. There is no basis for applying a lack of control or lack of marketability discount to an asset the market already prices continuously.

Q: Who should prepare the appraisal for a discounted Roth conversion? An independent, credentialed appraiser with no financial stake in the asset or its sponsor should prepare the report, following USPAP. An appraisal prepared by the fund manager, LLC sponsor, or promoter of the investment carries much less credibility if the valuation is ever questioned.

Q: Does a discounted conversion guarantee the IRS will accept the lower value? No. The IRS reviews these determinations on the facts and documentation presented. A well-supported, independent appraisal is prepared to support a defensible position; it does not guarantee acceptance of any specific discount percentage.

Q: How large does an IRA need to be for this to make sense? There's no fixed threshold, but the tax savings need to justify the cost of an independent appraisal and any legal review of the underlying agreements. For smaller accounts or modest discounts, the professional fees involved can outweigh the benefit.

Getting a Defensible Valuation Before You Convert

A discounted Roth IRA conversion is only as strong as the appraisal behind it. The mechanics are straightforward: an independent appraiser establishes a supportable, discounted fair market value for an illiquid SDIRA asset, that value becomes the taxable amount of the conversion, and everything the asset earns afterward grows inside the Roth IRA without additional tax on that appreciation. Getting the valuation wrong, whether too aggressive or simply undocumented, undermines the entire strategy.

If you're holding an LLC interest, real estate, or a closely held business stake inside a self-directed IRA and are weighing a Roth conversion, request an appraisal from our team to get an independent, USPAP-compliant valuation before you convert.

This article is provided for general informational purposes only and does not constitute legal, tax, or financial advice. Readers should consult a qualified attorney or CPA regarding their specific circumstances.